AI’s Hidden Bottleneck: Why Power, Batteries, And Infrastructure Are The Real Opportunity

From Algorithms To Amperes

For the last two years, the AI story has been told mostly through software releases, chip launches, and eye‑catching model demos. But as we move into 2026, the centre of gravity is shifting: the real constraint is power.

Large AI data centers run 24/7, drawing enormous amounts of electricity and requiring resilient cooling, land, water, and grid access. Governments and utilities are warning that existing power systems are struggling to keep up. For investors, that creates a structural opportunity in the “physical” layer of AI: energy, battery storage, and infrastructure assets that enable computers at scale.

This insight explores three linked themes: surging electricity demand from AI, the rapid growth of battery storage, and why infrastructure and real assets may offer more resilient exposure to the AI boom than simply owning megacap tech.

AI Is Rewiring Global Power Demand

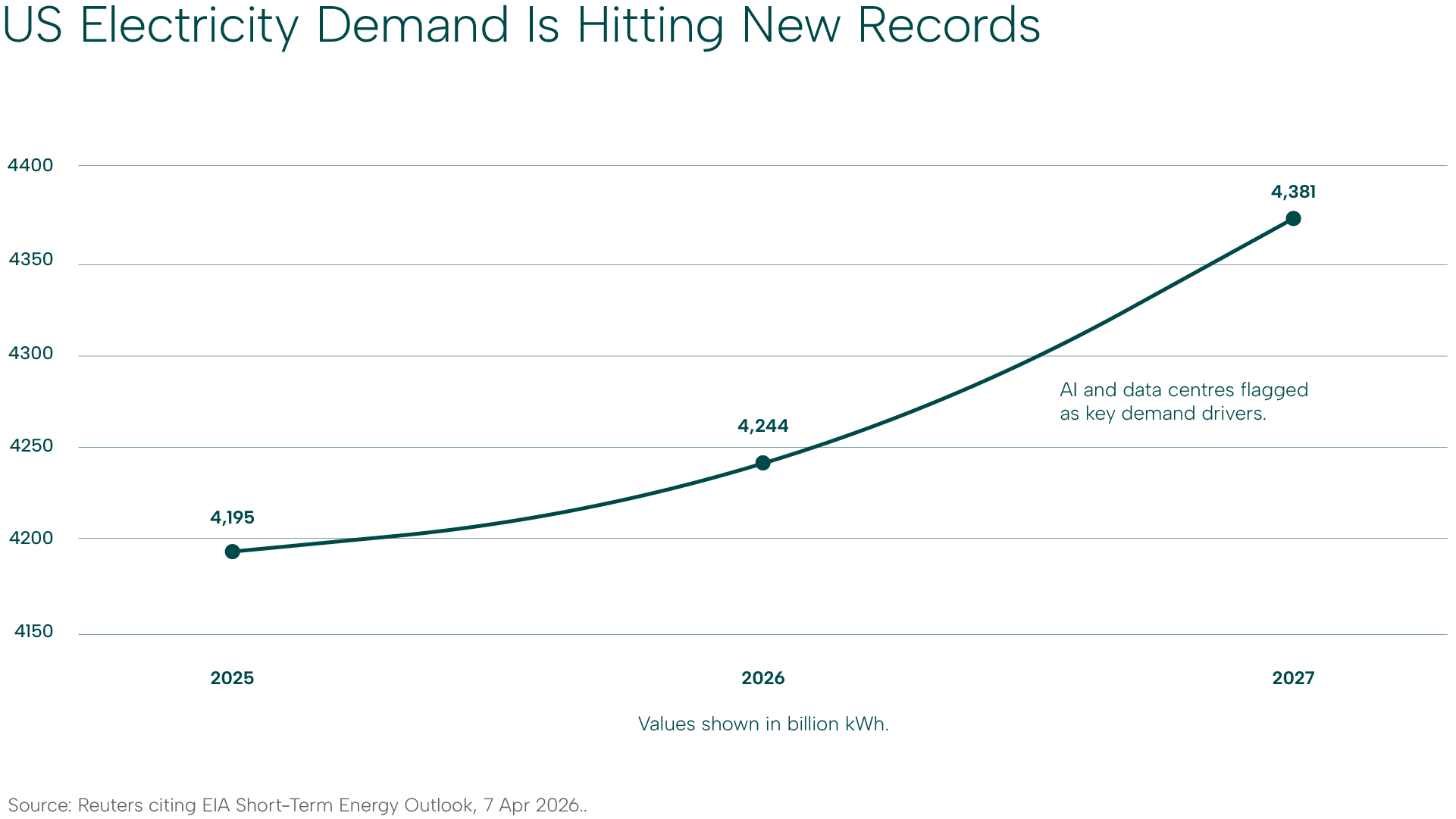

The US Energy Information Administration (EIA) now expects US electricity consumption – already at a record – to hit new highs in both 2026 and 2027. Power use reached roughly 4,195 billion kWh in 2025 and is projected to climb further as data centres and electrification drive demand.

The EIA explicitly cites AI and cryptocurrency data centres as key reasons why power use is rising, even as households and businesses move away from direct fossil‑fuel heating and transport. That is a structural rather than cyclical shift: once a data centre is built, it tends to run flat‑out for years.

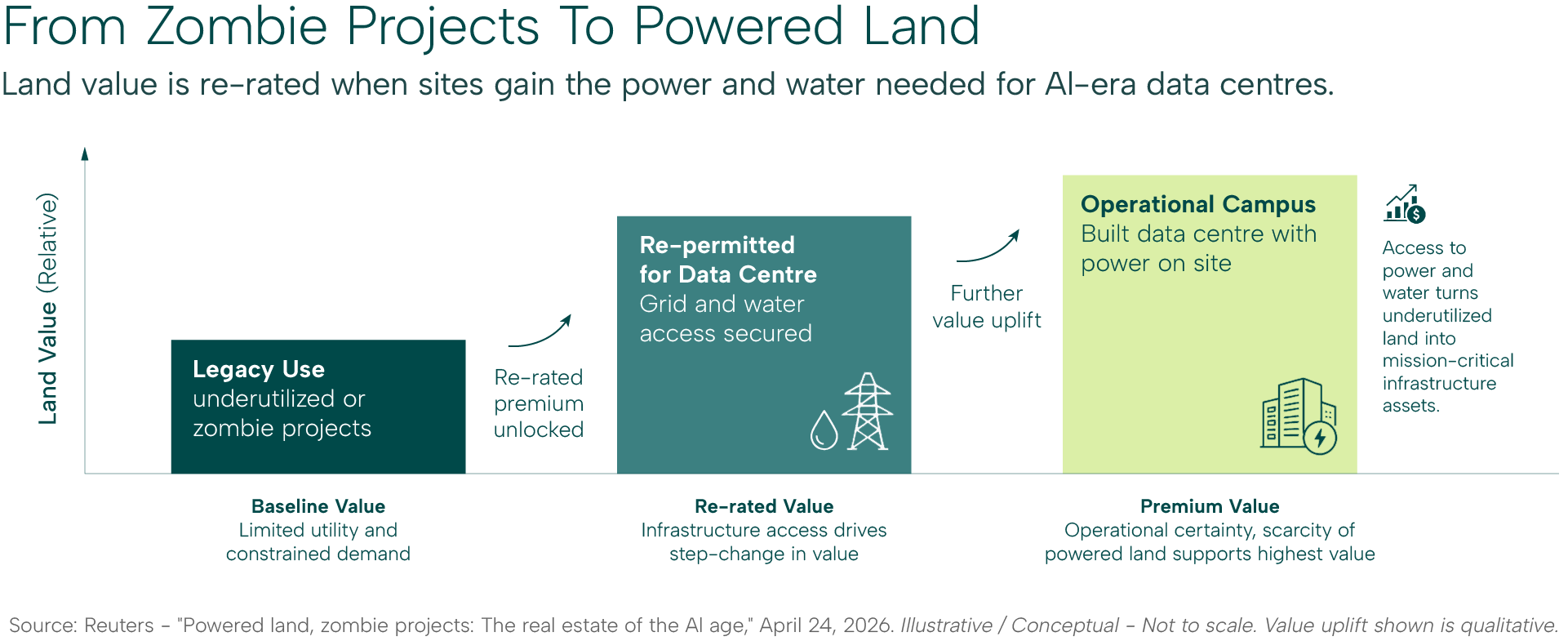

In Europe and the UK, a similar pattern is emerging. Reuters recently highlighted brownfield industrial sites in northeast England that have been reborn as prime locations for AI data centre campuses simply because they already have power plants, water access, and grid connections. Land that was once a “zombie project” is now valued for the megawatts it can deliver, not the buildings that sit on it.

On the investment side, Morgan Stanley estimates that US data centre power demand could reach roughly 74 GW by 2028, with an estimated shortfall of about 49 GW in available power access based on current project pipelines. That gap implies hundreds of billions in capital spending on generation, transmission, and on‑site energy systems over the next several years. Bedrockgroup

Battery Storage And Grids Are Scaling To Catch Up

Higher electricity demand would be challenging enough on an unchanged grid. But the shift toward renewables adds another layer of complexity: the sun and wind are intermittent, while AI workloads are not. That is where battery storage and grid technology come in.

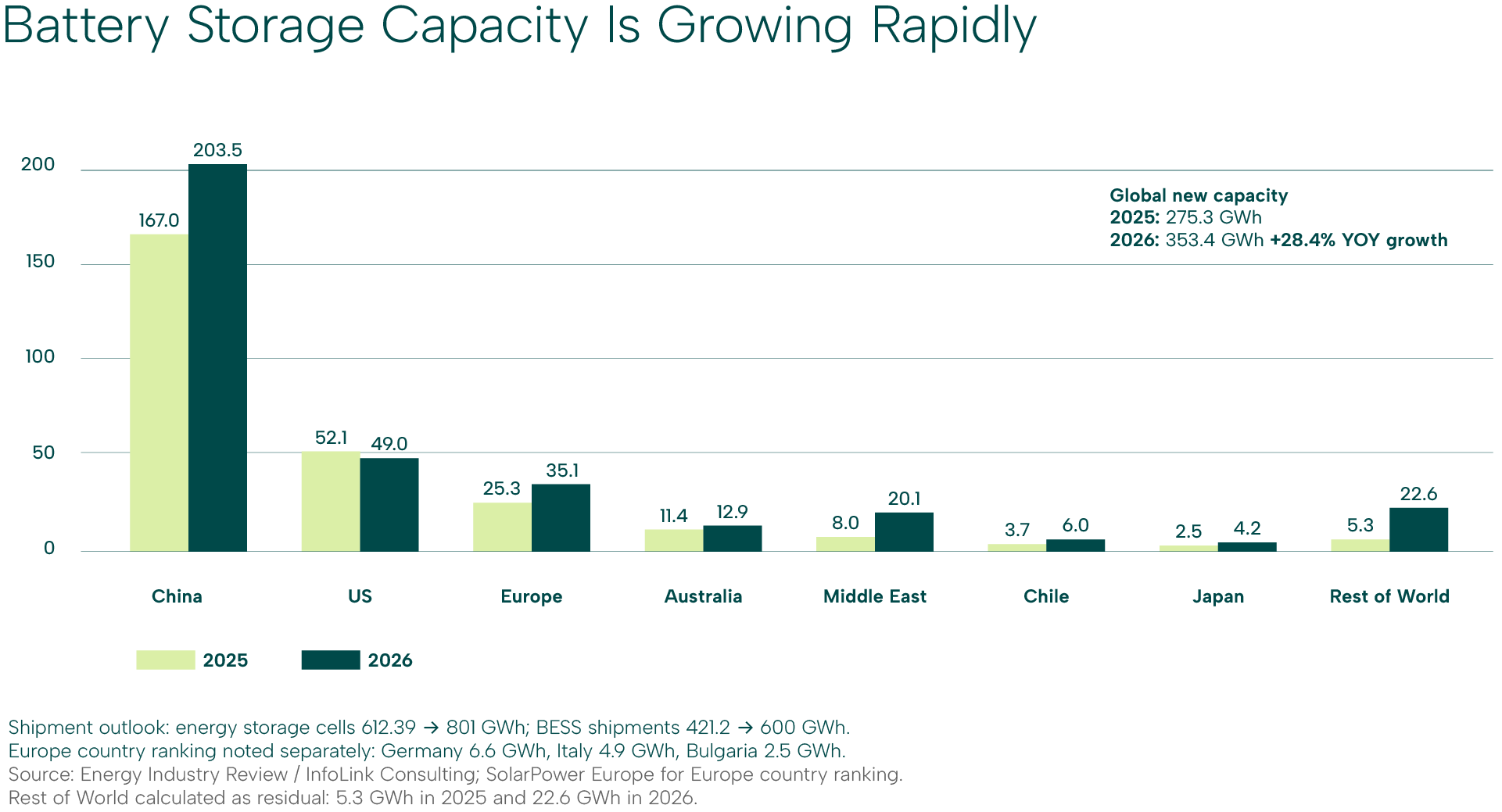

Global energy storage deployments are already growing at record speed. InfoLink Consulting reports that battery energy storage systems reached 275.3 GWh in 2025, up 61.3% year‑on‑year, and are expected to add another 353.4 GWh in 2026. China led with roughly 167 GWh of new capacity in 2025 and is expected to add over 200 GWh this year, while the US, Europe, and Middle East all show double‑digit GWh additions.

The World Economic Forum notes that over 15 GW of batteries were added to the US grid in 2025 alone, and sees storage increasingly deployed not just for arbitrage or backup, but as a network asset – a flexible buffer that relieves stressed transmission lines and stores surplus power when the grid is under‑utilised.

Energy storage analytics firms are now explicitly calling out AI as a new demand driver. Wood Mackenzie highlights data centres as one of the key trends in the 2026 global storage market, citing examples where facilities secured faster grid connections by installing battery systems to provide demand response and manage rapid load ramps. ess-news

AI, Climate Tech, and Infrastructure: A Converging Investment Theme

This is not just about keeping the lights on. It is accelerating a broader capital shift toward climate tech and infrastructure.

J.P. Morgan’s 2026 Climate Tech report points to rising electricity demand, grid congestion, and the need for storage and critical minerals as key themes shaping the energy transition. The report describes climate tech as an “industrial transformation”, with innovation in battery chemistry, grid software, and power‑system intelligence moving from pilot projects to commercial deployment.

Infrastructure managers are reaching similar conclusions. Franklin Templeton’s ClearBridge infrastructure outlook argues that AI data centres, decarbonisation, and network upgrades are all contributing to a robust multi‑year investment cycle in utilities and regulated infrastructure. They highlight that essential service assets – like power networks and pipelines – can offer resilient earnings through long‑term contracts even in volatile macro environments.

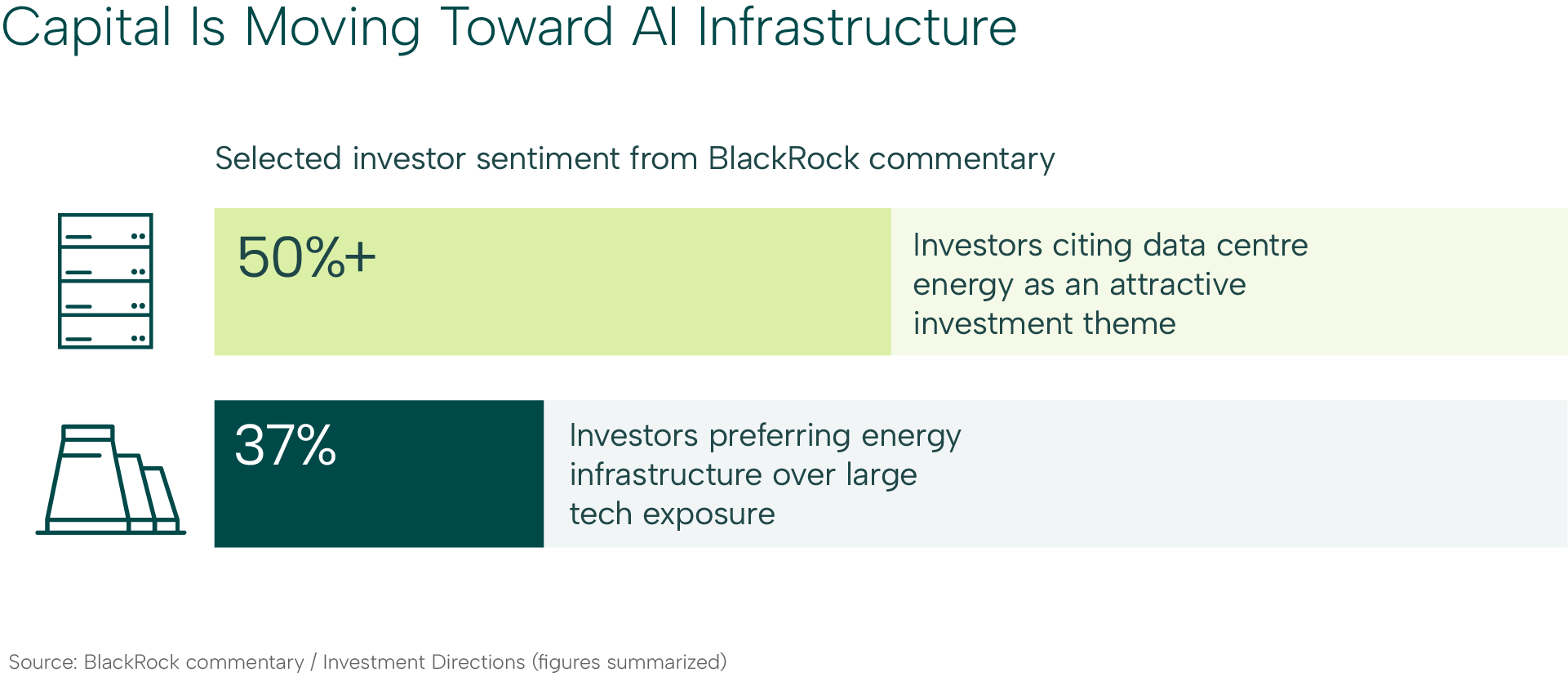

On the capital allocation side, BlackRock’s latest Investment Directions commentary notes that investors are “betting big on data centre energy”, with surveyed clients increasingly favouring energy infrastructure and grid assets over direct megacap tech exposure. More than half of respondents saw data centre energy as an attractive theme, and around 37% preferred energy infrastructure to large tech as their primary way to play AI.

Where We See Opportunity: Real Assets And Powered Land

The real estate and land angle is becoming more visible. Reuters has described “powered land” – sites with existing power plants, water, and grid connections – as a new sub‑sector in UK real estate, with abandoned industrial sites, former factories, and even old hotels being repurposed as potential AI data centre campuses.

As proposals for new AI data centres surge, grid connection queues and permitting have become the gating factor. Investors with access to strategic land parcels, substations, or brownfield sites with strong infrastructure are now in a position to command premiums.

This trend fits into broader infrastructure themes highlighted by asset managers: grid modernisation, onshoring, and resilience against climate and geopolitical shocks. For investors willing to take an active, long‑term approach, there is a window to acquire or back assets that may benefit from being “in the path of power”.

MYJ Insight

AI is still in its early innings, but the investment frontier is already moving beyond headline tech stocks. Surging electricity demand, rapid growth in battery storage, and the re‑rating of infrastructure and powered land are turning the “plumbing” of the digital economy into a core investment theme.energyindustryreview+2

For investors, the key questions are:

Where will power demand be most constrained?

Which grids and storage assets are best positioned to solve that constraint?

How can portfolios gain exposure to these trends without being over‑concentrated in a handful of megacap names?

MYJ Capital’s role is to help answer those questions with a disciplined, real‑asset lens – looking across infrastructure, energy, and strategic real estate that sits on the right side of this structural shift.

If you’d like to explore how AI’s power bottleneck could fit into your investment strategy, contact the MYJ team at myjcapital.com/contact for a confidential discussion, and subscribe to receive our latest real‑asset and infrastructure opportunities.