AI Infrastructure: The Next Frontier for Portfolio Growth

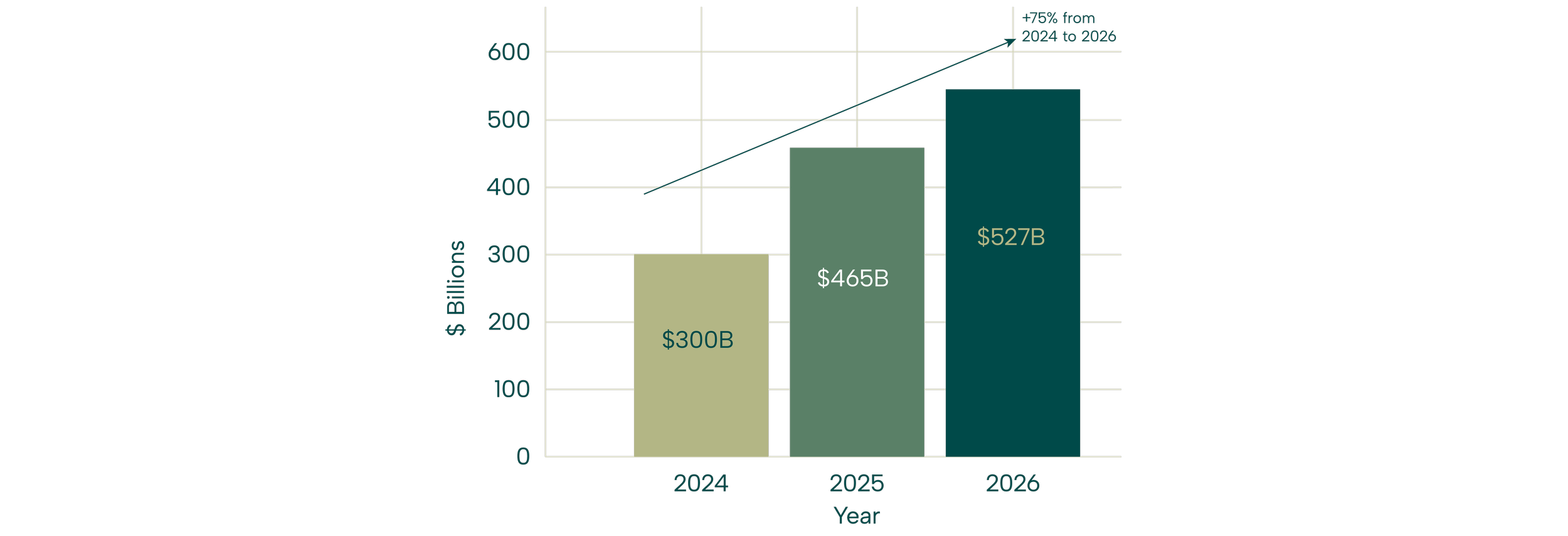

High-net-worth investors entering 2026 face a landscape defined by technological acceleration and policy tailwinds. Artificial intelligence has evolved from experimentation to enterprise adoption, driving unprecedented demand for supporting infrastructure—particularly data centers and power systems. With analysts forecasting AI-related capital spending to exceed $500 billion in 2026, savvy allocators are positioning in private equity vehicles targeting this "super-cycle" of digital and physical infrastructure. This shift offers resilient, high-conviction returns decoupled from public market volatility.

Surging AI Capex Fuels Infrastructure Demand

Global AI companies, led by hyperscalers, continue upwardly revising capital expenditure plans amid robust earnings. Consensus estimates now peg 2026 AI capex at $527 billion, up sharply from prior forecasts, as firms scale compute power for generative models and enterprise applications. Venture capital in generative AI alone hit nearly $50 billion in H1 2025, surpassing full-year 2024 totals. Data centers require $5.2 trillion in investments by 2030 to meet compute demands, creating a multi-year runway for private markets.

AI Capex Trajectory: Explosive Growth Powers Infrastructure Opportunities.

This capex surge intersects with energy transition themes from your prior insights, as data centers alone could double electricity demand in key markets like the US and Asia.

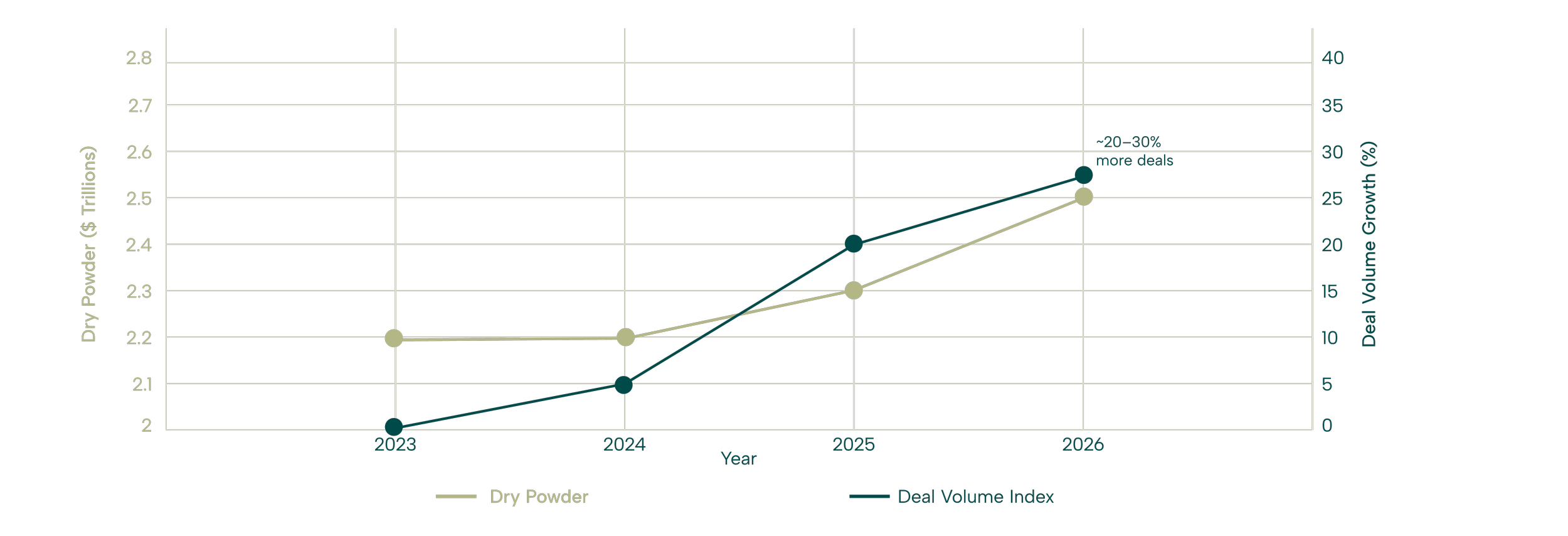

Private Equity's Prime Positioning

Source: Adams Street Partners, EY M&A Outlook

Private equity stands at the epicenter, with buyout activity accelerating on easing financing and narrowing valuation gaps. Median holding periods peaked above six years, pressuring general partners to pursue exits via IPOs and M&A—up 65% year-over-year. AI-native platforms and infrastructure plays dominate, as managers deploy operational AI for value creation in portfolio companies. High-net-worth individuals benefit from semi-liquid vehicles, drawing retail interest while maintaining access to mid-market deals yielding superior spreads.

US policy under President Trump amplifies this: Infrastructure Investment and Jobs Act funding flows through FY2026, with $72.6 billion requested for highways, freight, and grid modernization—ideal complements to AI power needs. Federal Highway Administration estimates support $64.1 billion in core programs, fueling public-private partnerships.

Strategic Allocation for High-Net-Worth Portfolios

For discerning investors, target allocations to AI infrastructure private equity—aiming for 15-25% in alternatives, per ultra-high-net-worth benchmarks exceeding 40%. Prioritize:

1. Data Center Developers

Firms scaling modular facilities with renewable integration, capturing hyperscaler leases.

2. Power & Grid Plays

Utilities and mid-market operators modernizing for AI-driven load growth.

3. AI-Enhanced Buyouts

Sector specialists in industrials and fintech leveraging AI for efficiency.

These assets offer inflation-hedged cash yields (6-9%) alongside 15-20%+ IRRs in upside scenarios, balancing growth with downside protection. Risks like regulatory scrutiny remain, but flight-to-quality favors experienced managers.

Source: goldmansachs | moonfare+1 | energytracker | adamsstreetpartners | spartnerships | titaninvestors | comerica | adamsstreetpartners | gurustartups+1

Positioning Ahead of the Curve

2026 marks a renaissance in private markets, where AI infrastructure converges with policy-enabled execution. High-net-worth investors who act now—via co-investments or dedicated funds—secure first-mover advantages in this trillion-dollar buildout.

MYJ Capital guides clients through these opportunities, blending conservative stability with dynamic upside.

Contact MYJ Capital to explore how AI infrastructure may impact asset allocation and risk positioning.

Connect with us at