Tech’s Wild Ride: What the AI Pullback Really Means

The latest drop in technology stocks was a reminder that even the strongest themes can stumble when valuations run ahead of conditions, financing costs rise, and investors are forced to reprice risk quickly. Reuters reported that the AI rally turned “ugly” in early June, with sharp losses across Asia and Wall Street as investors slammed the brakes on red-hot tech names.

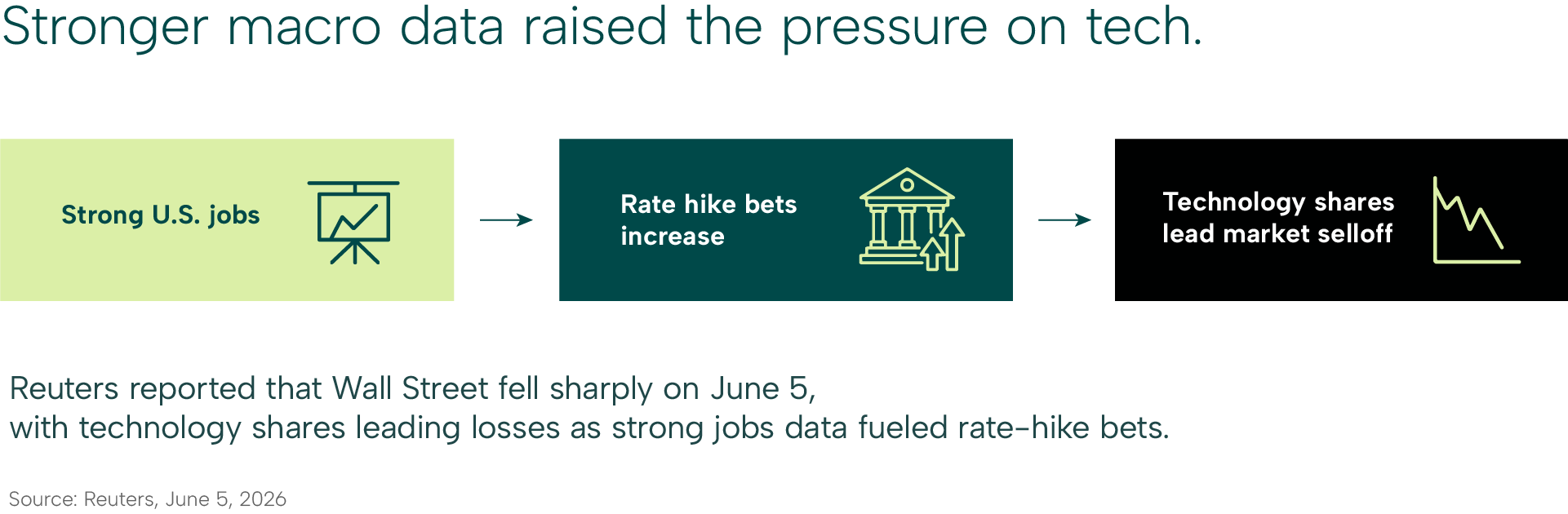

The immediate trigger was not a collapse in the AI story itself. Instead, it was the combination of strong U.S. jobs data, rising bond yields, and renewed concern that policy may stay restrictive for longer than markets had hoped. Reuters said Wall Street’s June 5 selloff was led by technology shares after strong jobs data fueled rate-hike bets, with investors moving out of high-duration growth names as yields rose. In practice, that matters because many AI-linked companies are still priced on expectations of future earnings. When discount rates rise, those future cash flows become less valuable today. Reuters

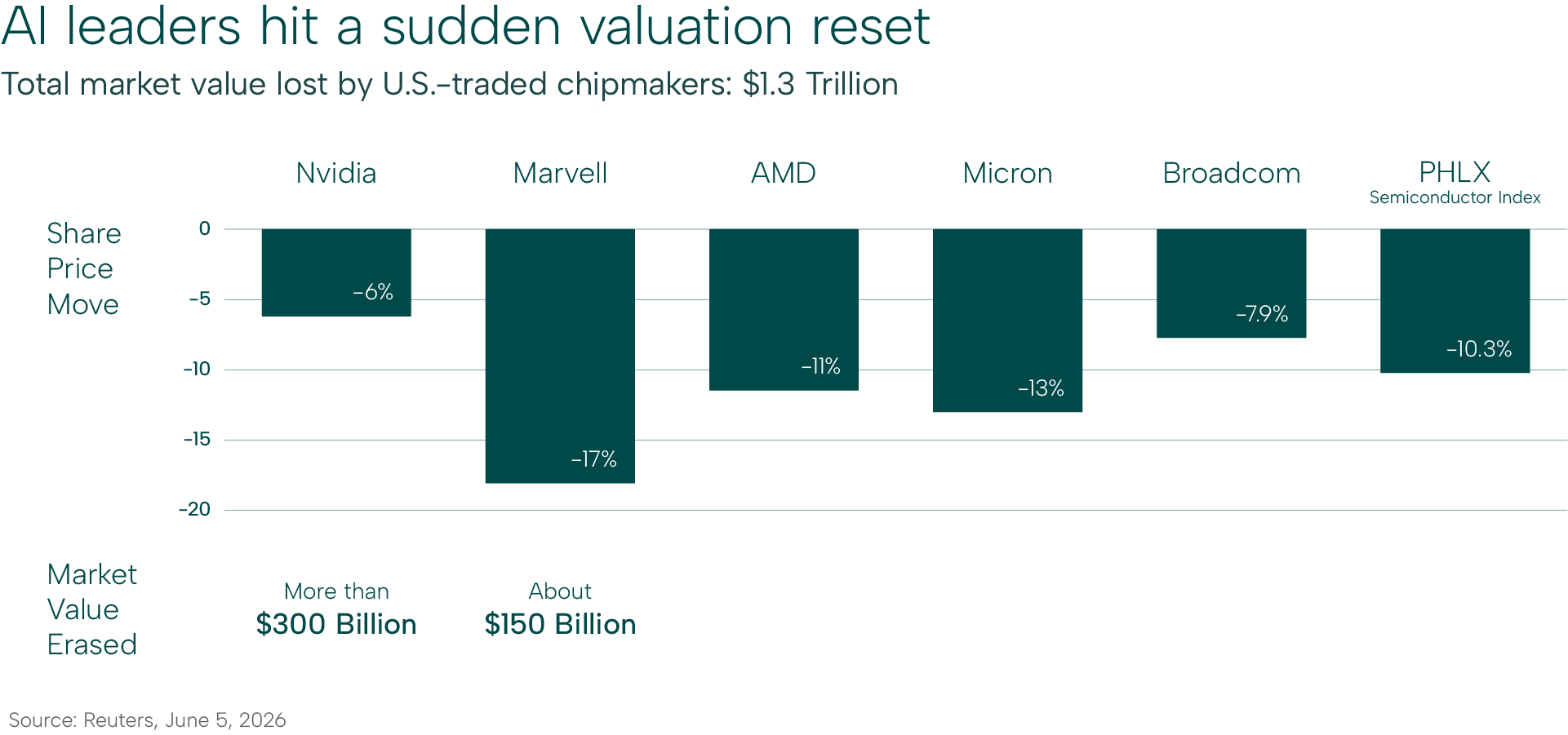

The scale of the move shows how concentrated the recent rally had become. Reuters reported that U.S.-traded chipmakers lost about $1.3 trillion in market value in the June 5 slump, with heavy losses concentrated in AI bellwethers. That kind of drawdown does not necessarily mean the long-term thesis is broken. It does show, however, that market leadership built on a narrow set of names can reverse quickly when sentiment changes. For strategic investors, that is less a reason to panic than a reason to distinguish between theme conviction and position sizing. Reuters

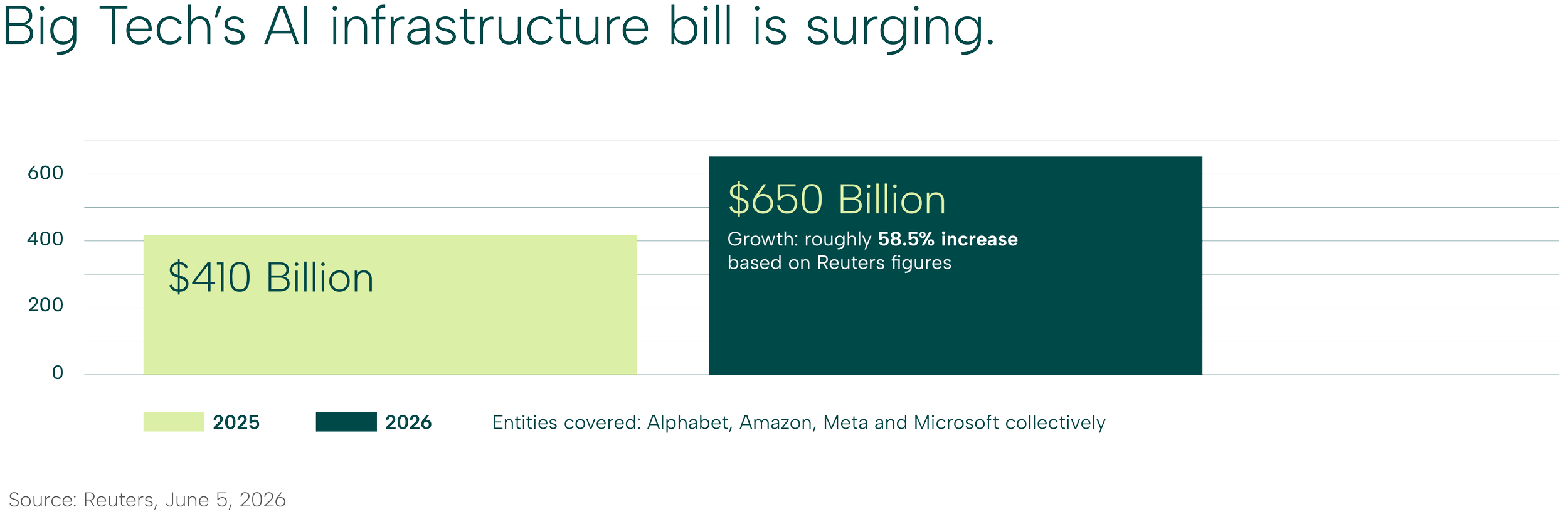

There is also a structural story unfolding behind the volatility. The AI build-out is no longer a speculative software trade alone; it is a capital-intensive infrastructure cycle. Reuters reported that Alphabet, Amazon, Meta, and Microsoft are expected to invest about $650 billion in AI-related infrastructure in 2026, up sharply from $410 billion in 2025. That spending has to be financed, and financing at this scale changes market behavior. When capital requirements surge, companies need more than earnings momentum and private capital enthusiasm. They need broader access to funding pools, including public equity and debt markets. Reuters

That is why the coming wave of public fundraising matters. If more frontier AI firms and infrastructure-heavy technology businesses tap public markets, investors may need to fund those purchases by trimming existing winners. The pressure is not purely fundamental; it is also mechanical. New issuance can absorb liquidity, especially when the same investor base has already crowded into a narrow leadership group. In that sense, the recent pullback may be less about rejecting AI and more about the market adjusting to the cost of financing it. Reuters

From MYJ Capital’s perspective, the key takeaway is that the market is moving from an excitement phase to a capital-discipline phase. In the first phase of a major theme, investors reward the boldest growth narratives. In the second, they start asking tougher questions: who can fund expansion efficiently, who can sustain margins under higher rates, and which parts of the value chain benefit even if headline leaders de-rate. This is where macro and market structure begin to matter as much as innovation itself.

The macro overlay is critical. Reuters noted that strong jobs data helped fuel concerns about higher interest rates, and that rising yields amplified pressure on technology favorites. When markets believe central banks will keep policy tighter, the valuation premium attached to long-duration growth assets becomes harder to defend. That does not mean tech becomes uninvestable. It means investors need to be more selective about entry points, funding risk, and balance-sheet resilience. Reuters

A second implication is that public markets may become more influential in shaping the next chapter of AI. For the past phase, capital was abundant and often private. The next phase appears likely to involve more public issuance, more investor scrutiny, and more competition for capital. Reuters’ estimate of $650 billion in AI infrastructure spending this year suggests the financing need is simply too large to remain a niche private-market story. As that capital demand broadens, market volatility around flagship tech names may become a recurring feature rather than a one-off event. Reuters

For investors, this environment argues for discipline over impulse. Pullbacks can create opportunity, but only when the underlying thesis survives tighter financial conditions and more demanding capital markets. The recent selloff does not disprove AI’s importance. It does remind investors that even transformative themes must still pass the tests of valuation, liquidity, and funding durability. The story is maturing from “AI at any price” to “AI with financing, selectivity, and macro awareness”. Reuters

MYJ’s broader insight is that this is a cross-asset story about rates, liquidity, issuance, and capital allocation. When technology becomes infrastructure, the winners are not only the companies with the best narrative, but the ones that can navigate tighter policy, absorb large capex cycles, and attract capital without destabilizing their own valuation base. That shift may ultimately make the AI trade healthier, but it also makes it less forgiving.