Supersized M&A in the AI Era: Reading the $2.8 Trillion Deal Wave

A record-breaking first half: fewer deals, much larger transactions

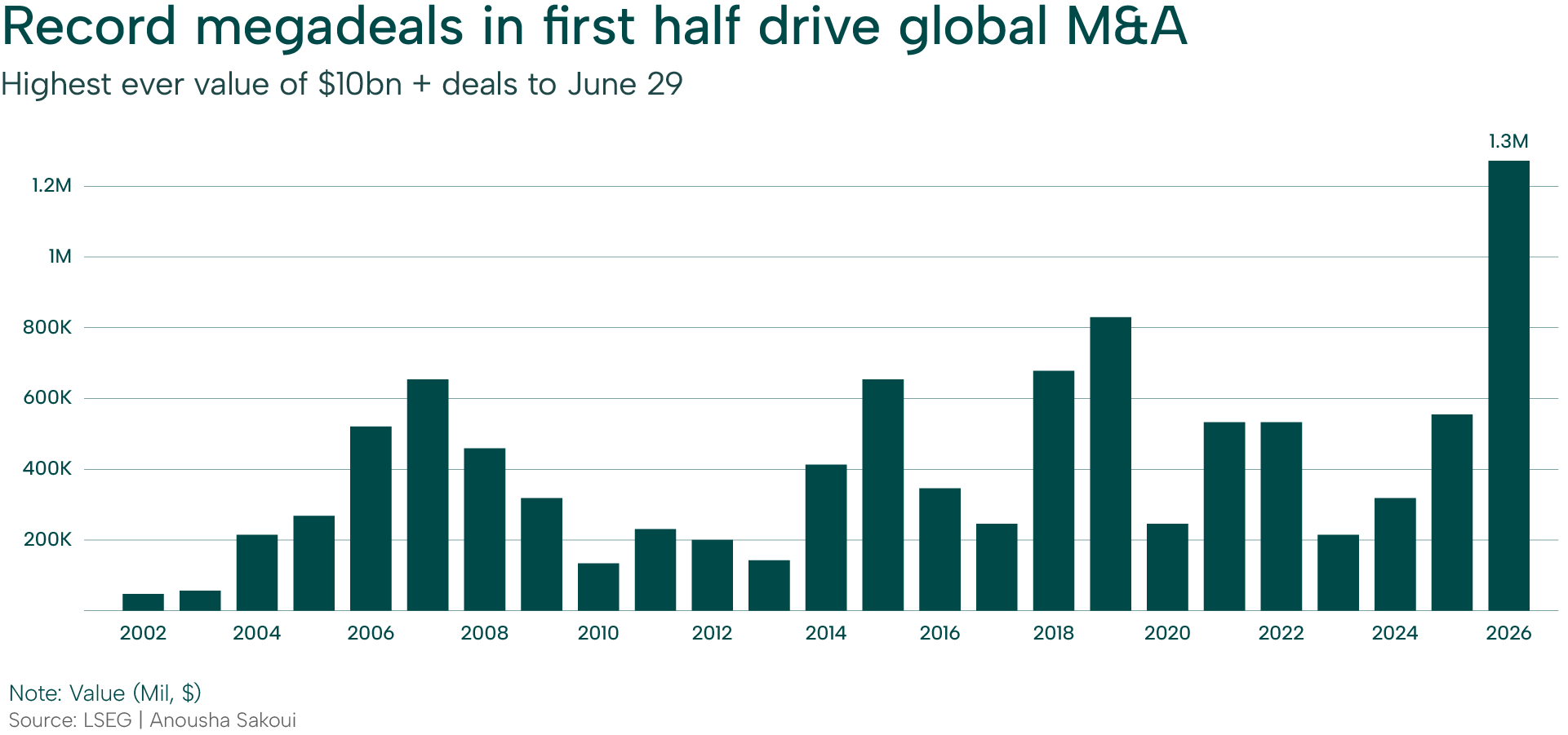

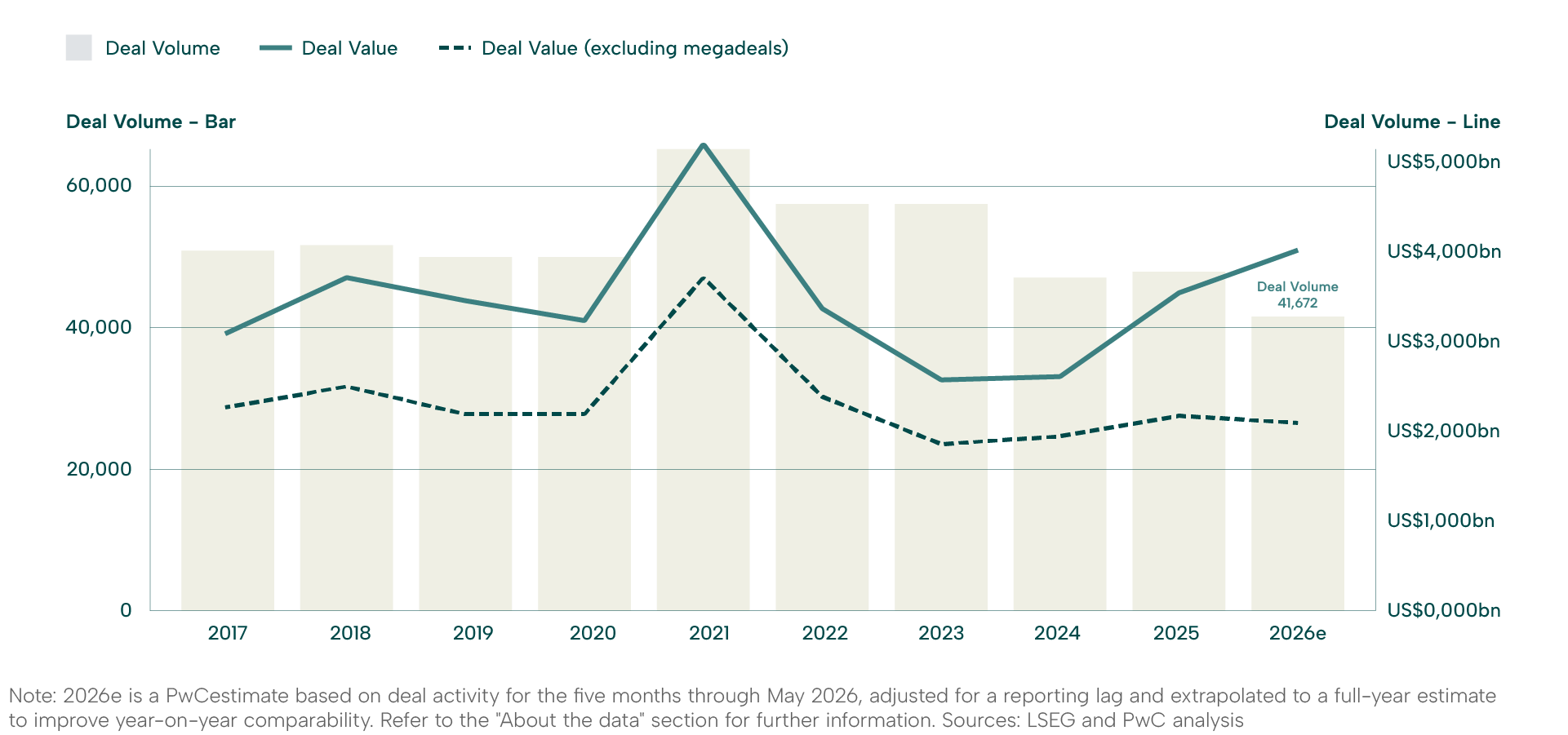

Global mergers and acquisitions reached an estimated $2.8 trillion in announced deal value during the first half of 2026, surpassing the previous high set in 2021 and marking the strongest first-half on record since LSEG began tracking the data. That total represents roughly a 48% year‑on‑year increase, even though the number of transactions fell by about 9% to around 24,000 – the lowest first-half tally in six years.

This combination of rising deal value and declining deal count points to a market dominated by large, transformational transactions rather than high-volume deal flow. LSEG data show that 47 megadeals with values above $10 billion together exceeded $1.3 trillion, accounting for close to half of total global M&A value in the period. The current cycle is therefore not just active; it is supersized. Source: Economictimes, LinkedIn

Financing the wave: corporate debt and HALO assets

The record M&A wave is underpinned by highly accessible acquisition financing. Global investment‑grade corporate bond issuance reached roughly $3.4 trillion in the first half of 2026, around 10% higher than the same period a year earlier, giving large, highly rated issuers deep and predictable funding pools for cash‑heavy offers and liability management.

Alongside this financing backdrop, advisory commentary highlights a growing focus on “HALO” investments – heavy assets, low obsolescence, and large infrastructure or industrial platforms. In a world where software and AI are reshaping business models, these assets can anchor cash flows in essential services and long‑dated projects: power generation, transmission networks, logistics assets, and capital‑intensive AI infrastructure.

Recent megadeals reflect this tilt toward scale and durability: NextEra Energy’s $66.8 billion merger with Dominion Energy, Unilever’s $66 billion sale of its food division, and SpaceX’s roughly $60 billion acquisition of Cursor are all examples of boards using large transactions to re‑shape portfolios for a different operating environment. Source: Finimize, PWC, Finance.biggo

Sector and regional dynamics: technology, AI, and the Americas

Sectorally, technology and AI remained the largest contributors to global deal value. LSEG data reported by Reuters show that technology led global dealmaking with about $649 billion of announced transactions in the first half of 2026, driven by investments in AI infrastructure, data platforms, and adjacent industries. PwC’s technology, media, and telecommunications mid‑year outlook notes that companies are using M&A, partnerships, minority stakes, and capacity agreements to secure access to compute, data, and talent across the AI landscape.

Regionally, the Americas – led by U.S. markets – captured a majority of global deal value while representing a smaller share of global deal volume, reflecting the concentration of megadeals in that region. PwC’s Global M&A mid‑year outlook highlights that the Americas accounted for a disproportionately high share of deal value despite a more modest share of deal count, while cross‑border M&A reached approximately $893 billion, up about 62% year‑on‑year, marking the strongest first‑half start since 2018. Source: PWC

These patterns suggest that capital is flowing into a combination of AI‑linked capability plays and large, regionally anchored platforms that can support scale and transformation agendas.

Strategic implications: how record M&A reshapes the investment landscape

The record $2.8 trillion headline and the surge in megadeals are not, in themselves, investment recommendations. They are signals about how boards, lenders, and regulators view risk, opportunity, and the pace of structural change. Bain and PwC both point to a market in which leading companies are using large transactions to reposition around AI, infrastructure, and HALO assets, while taking a more selective approach in other areas.

For investors, several implications stand out:

Valuation anchors and sector re‑ratings. Large, well‑publicized deals can reset valuation benchmarks within sectors, influencing not only listed peers but also private assets and pipelines. ft

Balance‑sheet strength and execution risk. Easy access to funding allows large transactions to proceed, but leverage levels, integration complexity, and regulatory scrutiny remain central to long‑term value creation.

AI and HALO assets as structural themes. Technology, AI, and long‑life infrastructure are emerging as core themes behind the biggest moves, suggesting where boards expect durable advantage to sit over the next decade.

Source: Bain, ft, PWC

MYJ insight Why it matters for investors:

At MYJ, the focus is less on individual deal headlines and more on how this supersized M&A environment interacts with macro conditions, capital flows, and long‑term value creation. A market built on megadeals and HALO assets implies that scale, access to funding, and AI‑enabled capabilities may increasingly differentiate winners from the broader market. For investors, that calls for careful attention to balance‑sheet resilience, strategic clarity, and the alignment between acquisition themes and underlying fundamentals.

To learn more about how MYJ Capital approaches megadeals, AI‑driven transformation, and long‑term positioning, visit our products and strategies overview page.

Disclaimer: This article is provided for informational purposes only and does not constitute financial, investment, tax, or legal advice. Investing involves risk, including the possible loss of principal. Readers should conduct their own analysis or consult a qualified professional before making any financial decisions.